The signs are clear.

As per Wolters Kluwer, AI adoption in accounting firms increased from 9% in 2024 to 41% in 2025.

That’s a 400% increase in just 1 year.

And the momentum isn’t slowing down.

ChatFin reports that 73% of firms plan on adopting AI in the next 2 years. But here’s where it gets even more interesting.

Finastra’s latest research shows that only 2% of financial institutions claim they don’t use AI at all.

Let that sink in for a moment.

In the financial services domain, AI isn’t just on the horizon. It’s here- it’s part of the operations.

And accounting firms are under the same financial umbrella. So they are under external pressure to embrace AI-enabled accounting solutions – it’s equally about staying competitive externally as it is about keeping up internally.

What’s AI in accounting, really?

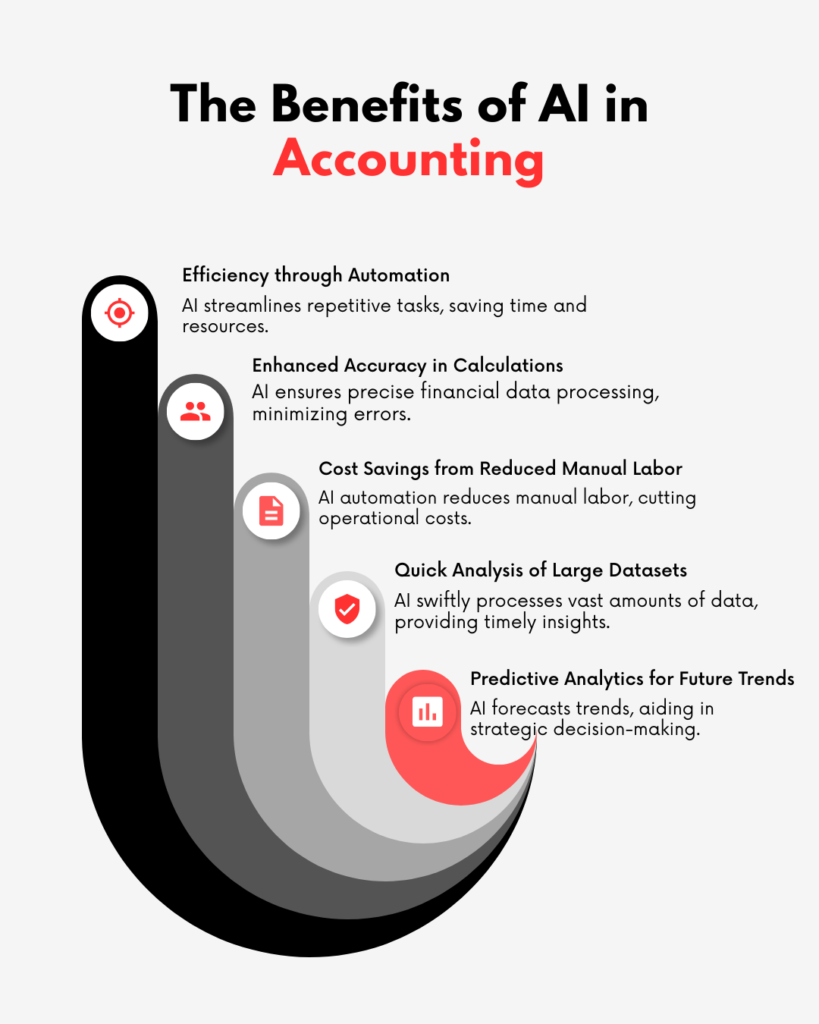

When you hear “AI in accounting,” think of smart tools- stuff like AI-powered accounting software, machine learning for audits, and automated bookkeeping.

There’s generative AI that can whip up financial reports, predictive analytics that spot trends and issues before they blow up, and tax tools that handle compliance headaches. These aren’t just fancy add-ons. They let accountants fly through mountains of data, catch weird transactions, and reconcile accounts in real time. What used to take hours, AI now does in minutes.

Audits? Machine learning doesn’t just sample a few transactions- it checks them all.

That means fewer mistakes, faster results. Generative AI can sketch out financial summaries, point out what matters, and even help with compliance paperwork. Predictive analytics can warn you about cash flow dips or revenue swings before they hurt.

So what’s left for accountants? A lot, actually!!!

Instead of drowning in paperwork, they get to focus on what really matters: smart analysis, strategy, and giving clients good advice. AI isn’t here to take over. It’s here to handle the boring stuff and make accountants even better at their jobs.

Let’s be clear

“AI doesn’t replace accountants. It upgrades them.”

What is fueling the rapid advancement of AI?

There are three reasons we can attribute the rapid advancement of AI.

Let’s explore these reasons.

1. Problems Are Being Solved by Automation: Accounting teams are tasked with:

1. Data entry

2. Errors with reconciliation

3. Running compliance audits

4. Documentation on compliance

5. Reporting

These are all tedious tasks that take a long time.

Automated AI can now do the following:

1. Processing invoices,

2. Detecting fraud,

3. Driving expenses,

4. Matching transactions, and

5. Drafting financial statements.

This is what accounting automation is, and it is here to SAVE TIME. If firms can see productivity increases, the case for automation becomes quite clear.

2. Client Financial Insights are Expected by the AI clients. No longer want to wait for an update four times a year. Here are the expectations today:

1. Immediate updates

2. Predictive cash flow

3. Improved financial plan based on data

4. Analysis of potential risks

This is where accounting becomes predictive through AI analytics.

AI tools analyze a company’s financial history to generate data-driven recommendations and predictive reports. From there, accounting firms make the transition from compliance work to strategic management. These management services are where the money is.

The AI Tipping Point: A Broader Financial Shift

Think about where we are right now. Just last year, AI was still this shiny, experimental thing.

Fast forward to 2025 – suddenly, everyone’s using it.

By 2026? People won’t just expect you to have AI; they’ll wonder what’s wrong if you don’t. It’s kind of like what happened with cloud accounting. Once, it was cutting-edge. Now, if you’re not in the cloud, you look behind the times.

AI’s heading down the same road.

So by 2026, if your firm isn’t using AI-powered bookkeeping, automated audit tools, or smart tax compliance systems, you’re not just missing a trend- you’re starting to look slow.

And it’s not about skill. It’s about keeping up with how fast things move, how much more efficient these tools make you.

Finastra’s research spells it out: we’ve hit a true tipping point for AI in finance.

Nearly every bank and financial firm has some version of AI in play now.

It’s running quietly in the background – helping with banking operations, sniffing out fraud, managing risk, making sure you’re following the rules.

Sure, cybersecurity and data privacy worries are real, but the gains from AI are just too big to pass up, so firms keep pushing ahead.

And it’s not just about doing things faster.

PwC’s new predictions say AI is actually changing the way businesses work. Firms using generative AI in finance and accounting aren’t just boosting productivity- they’re making better decisions, building smarter strategies.

With AI accounting software, machine learning in audits, and automated tax tools, companies are cutting costs, growing their advisory services, and giving clients insights that really matter. This isn’t just a tech upgrade. It’s a whole new way of working.

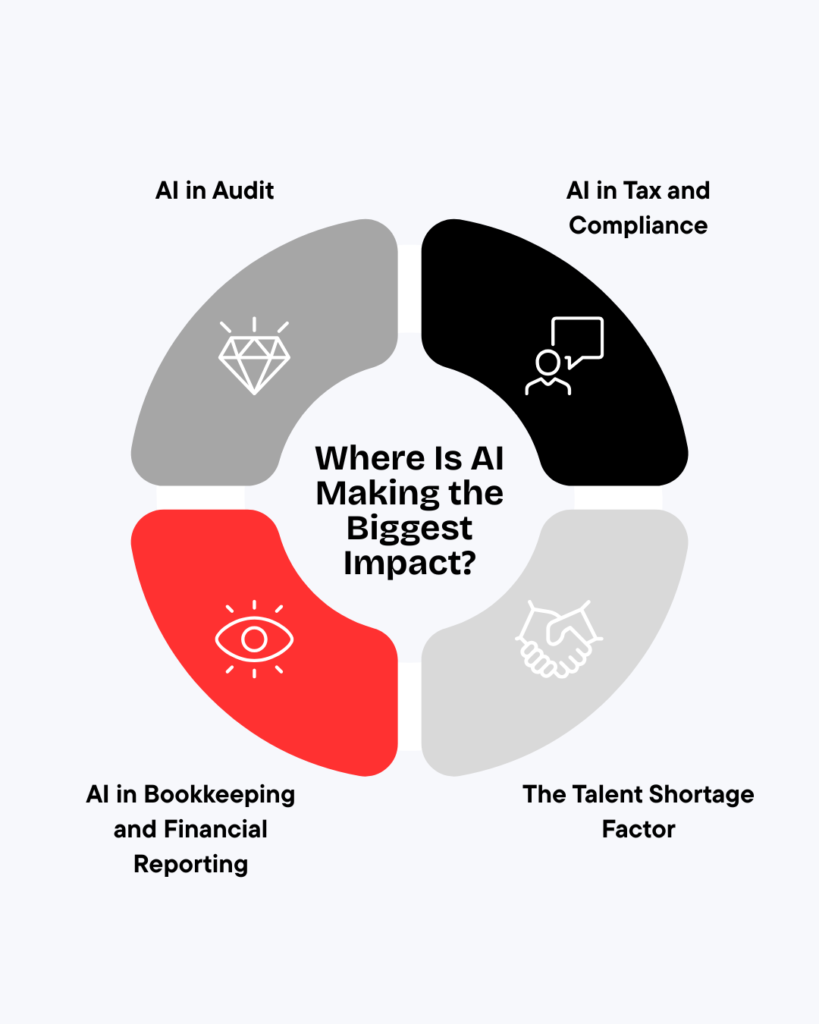

Where Is AI Making the Biggest Impact?

Let’s dig in.

- AI in Audit

Auditors used to check just a handful of transactions. With AI, they can scan every single one. That means, instead of looking at a tiny sample, firms now review everything- 100% of the data. The result? Better audits, sharper risk detection, and tighter compliance.

Machine learning even spots oddities in seconds. That’s a real shift.

- AI in Tax and Compliance

Tax research used to drag on for hours. Now, generative AI can quickly sum up tax rules, draft memos, and flag key compliance updates. Accountants work faster, and deadlines don’t feel as brutal. As tax rules get more tangled, AI-powered automation isn’t just helpful- it’s essential.

- AI in Bookkeeping and Financial Reporting

Bookkeeping has changed, too. Automated software now sorts transactions, matches payments, finds mistakes, and even puts together draft financial statements.

Everything runs faster, smoother, and on a much bigger scale. For small and mid-size firms, this is a huge time-saver.

- The Talent Shortage Factor

There’s one more thing- talent is running thin.

Fewer people are becoming accountants, and veteran CPAs are retiring.

Firms feel the squeeze. AI tools let smaller teams handle bigger workloads without burning out. Instead of piling on more staff for routine chores, firms automate, standardize, and tighten up their controls.

Accountants don’t vanish- they just get to focus on the work that really matters. AI gives them more impact.

Common Concerns Around AI in Accounting

AI is advancing rapidly in accounting, but people still have real concerns. And, honestly, they’re not wrong. These issues deserve real answers, not just quick fixes.

1. Data Security and Privacy

Money talk is always private, and financial data is especially sensitive. When firms start using AI for accounting, they have to lock down client info at every step.

What keeps folks up at night? Things like:

– Data breaches and cyberattacks

– Unauthorized people poking around in the system

– Shaky third-party vendors

– Figuring out if data can legally cross borders

– Keeping up with strict rules like GDPR, SOX, and other local laws

So how do firms protect themselves? They need:

– Solid, enterprise-level AI platforms

– End-to-end encryption for all data

– Multi-factor authentication and tight access controls

– Regular security audits and tests that try to break in

– Clear policies on who owns and manages the data

Many AI accounting tools put security front and center. But let’s be honest: tech alone doesn’t cut it. Firms still need to do their homework, vet vendors, and keep their own IT teams sharp. Security isn’t a “nice-to-have”- it’s the foundation.

2. Accuracy, Bias, and Reliability

AI is only as good as the data it learns from. Bad data? Bad results. Here’s what that means in real life:

– Transactions get misclassified

– Tax rules get misunderstood

– Algorithms show bias when assessing risk

– People start trusting the output too much, letting their guard down

Sure, machine learning and AI speed things up—especially in audits and taxes. But someone still needs to keep an eye on things.

Best practices look like this:

– Validating models regularly

– Checking the quality of incoming data, all the time

– Keeping clear records of how AI makes decisions

– Reviewing AI performance, not just once, but over and over

AI speeds up work, but it doesn’t eliminate risk.

3. Human Oversight and Professional Judgment

AI can spot patterns. What it can’t do is think like a pro or ask tough questions.

That’s why people still matter for:

– Reviewing financial statements

– Making final audit calls and materiality judgments

– Navigating tricky tax situations

– Deciding what’s ethical

– Giving clients advice they can trust

The smartest firms treat AI as a tool- not a boss. Let AI crunch numbers and sort the routine stuff. Accountants still need to own the big decisions.

4. Regulatory and Ethical Considerations

AI is everywhere in accounting now, so regulators are watching closely.

Firms can’t ignore:

– Being transparent about how AI makes decisions

– Keeping clear audit trails for everything the AI does

– Following new AI rules as they come out

– Using generative AI in a way that’s ethical and above board

\The right way to do this? Set up strong governance frameworks, define who’s in charge of what, and keep checking for compliance.

If you skip the rules, you open yourself up to trouble. But if you get governance right, you give your firm a real edge.

Is AI replacing accountants? People ask this all the time.

Let’s just say it straight: No, it’s not!!

AI is shaking things up in accounting, for sure. But it’s not pushing accountants out the door. Instead, it takes care of the boring, repetitive stuff- data entry, matching transactions, catching weird outliers, and making rough drafts of reports. Work gets done faster, and mistakes are fewer. Still, speed can’t replace good judgment.

That’s where accountants step in. They do what AI can’t touch:

STRATEGY.

INTERPRETATION.

REAL ADVICE.

ETHICAL CALLS.

BUILDING RELATIONSHIPS WITH CLIENTS.

Here’s where human-in-the-loop AI comes into play. Platforms like Kandor AI emphasize AI working alongside human experts. The technology augments decision-making, while trained professionals validate outputs, apply regulatory understanding, and provide contextual insight.

Honestly, as firms bring in more AI, they need even more sharp minds for high-level advice. With routine tasks automated, accountants can focus on big-picture consulting, forecasting, risk management, and strategic planning.

The job is changing, no doubt!!

It’s more analytical now. More about offering real advice. More about bringing value. But it’s definitely not going away.

Final Thoughts: Will You Lead the Change or Chase It?

AI in accounting isn’t creeping in- it’s racing. Last year, just 9% of firms used it. Now?

That number jumped to 41%. And most firms, about 73%, say they’re getting on board soon. This isn’t some slow-moving trend. It’s a real surge.

Look around the financial world. AI isn’t just a buzzword anymore. Firms are putting real money into audit automation, smarter financial reporting, and sharper data analytics. The path forward is obvious.

Get moving now, and you give yourself time to test things out, iron out the hiccups, and build something solid. Wait too long, and you’ll end up scrambling to catch up.

So, what’s your approach? Dabbling with AI here and there? Or laying out a real plan for the future? Because this shift-it’s not waiting for anyone.