Let’s face it: you didn’t become an accountant to fight cybercrime.

You’re here to help clients make good financial decisions, not to ward off ransomware attacks.

But here’s the truth: if you handle customer financial information, you’re already a target.

Accounting firms are seen by cybercriminals as a gold mine for sensitive information such as Social Security numbers, bank account information, payroll data, and tax filings. A single breach can result in dozens (or hundreds) of client records.

Why Cybersecurity in Accounting Isn’t Optional

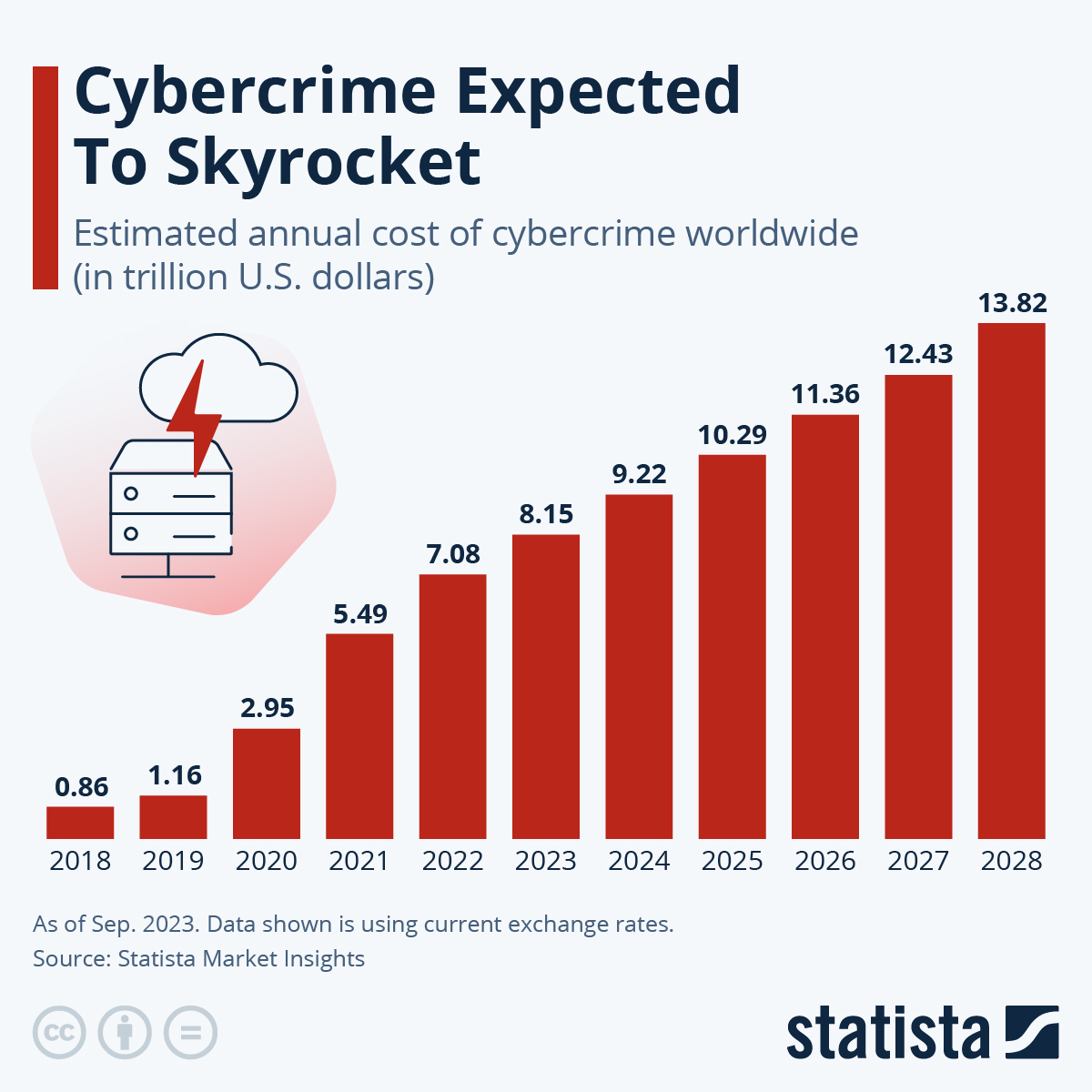

Cybercrime is no longer an abstract IT department concern.

It’s a matter of business survival. And the figures validate it:

$10.5 trillion – Projected global cybercrime costs by 2025 (Source: vikingcloud.com)

300% – Increase in cyberattacks on accountants since 2020

Every 40 seconds – Frequency of a cyberattack worldwide

Whether you’re a solo CPA or part of a mid-sized accounting firm, accounting data security is now central to client trust — and your reputation.

Why Accountants Are Prime Targets

Why Accountants Are Primary Targets

Hackers value efficiency. Why target individual taxpayers one by one when they can compromise the entire CPA company database?

On the dark web, each file might be worth hundreds (if not thousands) of dollars.

One breach equals dozens of paydays for fraudsters.

Think about what you store.

1) ID and Social Security numbers

2) Bank account and payroll data

3) Tax returns span years.

4) Corporate financial statements

Each file is worth hundreds (sometimes thousands) of dollars on the dark web.

One breach = dozens of paydays for cybercriminals.

Why Accountants Must Care About Cybersecurity

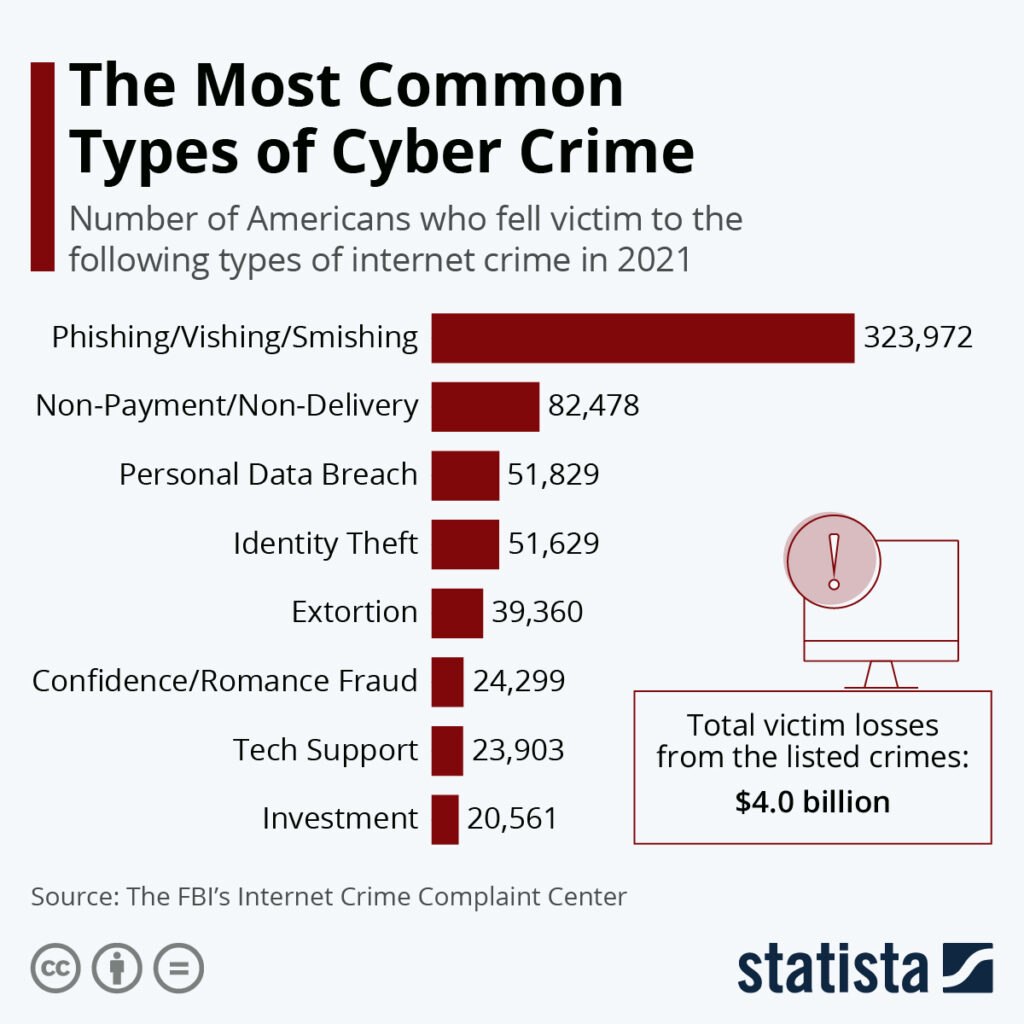

Your clients’ data is gold. Phishers, hackers and fraudsters know that your books contain juicy personal info: IDs, salaries, bank accounts and payroll data. That makes your firm a prime target. Common cyber threats include:

- Phishing & Social Engineering – Fake emails or links that trick staff into revealing passwords or downloading malware.

- Ransomware – Malicious software that encrypts your files and demands a ransom to unlock them.

- Weak Passwords – Reusing simple passwords across accounts is an open door for attackers.

- Unsecured Networks – Public Wi-Fi hotspots or poorly secured routers can be exploited.

- Outdated Software – Missing patches leave systems vulnerable to known exploits.

- Insider Risks – Even a staff mistake or an insecure vendor connection can open the door to hackers.

Trust is everything in accounting. A single breach can cost you clients and your good name.

A stolen tax record can sell for up to $1,000 on the dark web. Now multiply that by your client list.

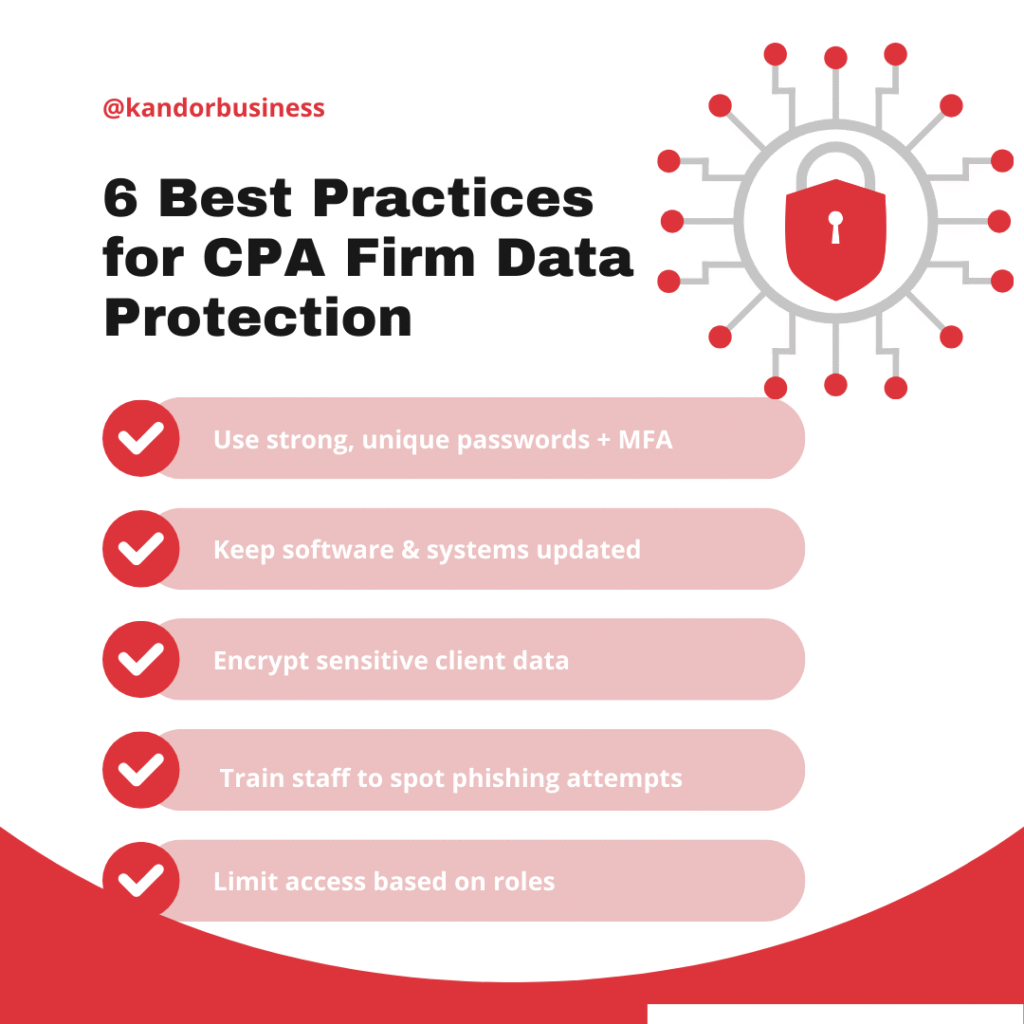

6 Best Practices for CPA Firm Data Protection

You don’t need a seven-figure IT budget to establish effective defences. You must develop consistent, sensible practices.

1) Apply the 3-2-1 Backup Rule.

- 3 copies of your info

- 2 different storage formats.

- 1 copy offline or offsite.

This assures that even if ransomware strikes, you may resume operations without spending a dime.

2) Strong passwords and multi-factor authentication

Consider your password to be the security lock on your office door. Multi-factor authentication (MFA) is the deadbolt. To avoid using the same credentials, use both—and a password manager.

3. Encrypt Everything

Full-disk encryption for laptops, smartphones, and USB drives is non-negotiable.

Even if a device is stolen, encryption renders the data useless without the key.

4. Secure Your Network

- Use a VPN on public Wi-Fi

- Enable WPA3 encryption on office Wi-Fi

- Update router firmware regularly

- Install a firewall

Cloud security for accounting firms starts with a secure local network.

5. Limit Access

Not everyone in your firm needs access to every client file.

Grant permissions on a need-to-know basis and revoke them immediately when staff leave.

6. Train Your Team

Your staff can be your biggest vulnerability — or your first line of defense.

Run quarterly security refreshers so phishing scams and suspicious links get caught before they cause damage.

Why Encryption Is Your Secret Weapon

Data encryption scrambles information so it’s unreadable without the key.

Use it for:

- Email attachments

- Client file transfers

- External backups

Most reputable cloud accounting software offers bank-level encryption, but encrypting before upload adds another security layer.

Cloud Backups and Recovery

The safest secure bookkeeping practices combine cloud backups with offline storage.

Follow the 3-2-1 rule with at least one physical copy stored offsite.

Test restoration regularly — a backup is useless if it won’t load when needed.

Outsourcing to a Secure Accounting Provider

Building in-house cybersecurity is costly and time-consuming.

Outsourcing to a provider with CPA firm data protection measures in place can save time, money, and risk.

Ask potential providers:

- Do you encrypt data at rest and in transit?

- Do you run regular security audits?

- What’s your backup and disaster recovery plan?

- Do you hold SOC 2 or ISO 27001 certifications?

If they can’t answer confidently, keep looking.

Your Cybersecurity Toolkit

The “Big Three” for accounting data security:

- Data Encryption – Use at least 256-bit for maximum safety.

- Cloud Backups – Automatic, secure, and compliant with accounting standards.

- Fraud Detection Software – Flags unusual transactions before they escalate.

Small accounting firms with a documented cybersecurity plan are 50% less likely to suffer a data breach.

The Big Picture: Cybersecurity Is About Trust

Cybersecurity in accounting is not just about technology — it’s about credibility.

Your clients trust you with their most sensitive information. A breach doesn’t just cost money; it costs relationships.

Embed security into your daily operations:

- Lock it down (strong access controls)

- Back it up (cloud + offline)

- Train your people (awareness first)

When clients know you take accounting data security seriously, you protect both their finances and your firm’s reputation.

Cybersecurity is a continuous journey. Technology and threats evolve, so make security part of your routine. Keep learning (follow industry news and training), and update your policies regularly. Conduct annual reviews or audits of your systems to spot hidden gaps. Consider cyber insurance as a last line of defense.

It won’t replace good security, but it can soften the financial blow if the worst happens. Accounting is a trust business. By embedding security into your practice – with encryption, backups, strict controls and smart outsourcing – you protect your clients and your reputation. The best time to stop a breach is before it happens.

The Bottom Line

Cybersecurity in accounting isn’t a “tech problem.”

It’s a trust problem.

Your clients trust you with their most sensitive financial information.

One breach can destroy that trust — and your reputation.

So…

- Lock it down

- Back it up

- Train your people

- And if you need help, partner with someone who lives and breathes secure accounting.

In today’s world, safeguarding client data isn’t just part of the job — it’s the whole job. That’s where Kandor helps you stay secure.